06 November, 2020

Uncategorized Archives - Page 38 of 62 - Raiz Invest

05 November, 2020

Bombarded by percentages all week? It can be enough to make even the financially savvy a little dizzy…

From the RBA lowering the cash rate from 0.25% to the lowest level in Australian history at 0.1%, to the percentage count of the US election results, there is a lot of information to process.

01 November, 2020

2/11/20

George Lucas, Raiz Group CEO

Global equities have just suffered their worst week since the market volatility in March when investors finally realised the full health and economic consequences of COVID-19. The market is attributing the sell-off to caution over the escalation in coronavirus cases and the US election, with the US tech titans the latest casualties in this selling.

31 October, 2020

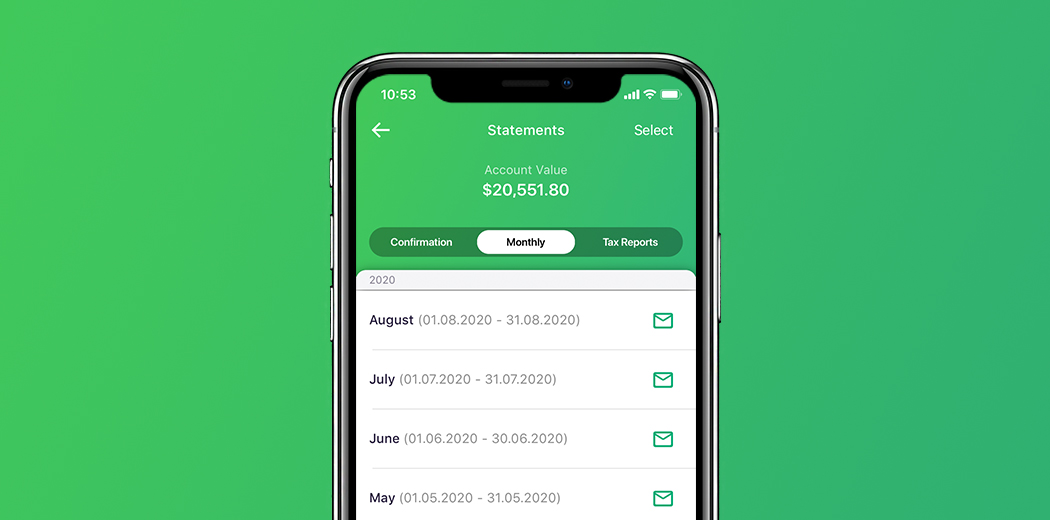

Over the past few weeks, we’ve been rolling out an update to your performance graph, giving you more information than ever before on the progress of your Raiz account.

30 October, 2020

When it comes to managing your money, there are many quick and easy ways to start on the path to getting control of your finances. Here are five of the best.

26 October, 2020

26-10-20

George Lucas, Raiz Group CEO

The US is under the investor microscope at the moment, with markets being driven by the ongoing Washington deadlock over a new round of stimulus and the likelihood of a deal being brokered before the November 3 elections. At the same time, focus continues to be on the COVID-19 situation in the US as case numbers rise and some states report that hospitals are under strain.

23 October, 2020

It’s commonly said that it takes money to make money. That is effectively true – those who live payslip to payslip with no spare cash have little to re-invest or save for a rainy day. However, if you take the time to re-evaluate your finances, you’ll realise that setting aside even the smallest of dollar amounts can really add up over a lifetime.

22 October, 2020

Start your Christmas shopping early with Raiz Rewards. For the rest of the month we will deposit a bonus $2 into your Raiz or Raiz Super account for every single Raiz Rewards purchase you make over $20. For more information on Raiz fees, click here.

20 October, 2020

We quietly achieved in the first three months of the 2020-21 financial year, with these achievements giving us grounds for optimism that the growth Raiz is enjoying will remain on track. Considering the global COVID-induced recession, this is a notable achievement of which I am immensely proud.

12 October, 2020

12-10-20

George Lucas, Raiz Group CEO

Last week saw China’s currency stage its biggest rally in 15 years, spurred on by a wave of foreign demand for Chinese assets and rising expectations that a victory by Democratic hopeful Joe Biden in next month’s US presidential election could help reset relations between the two superpowers.