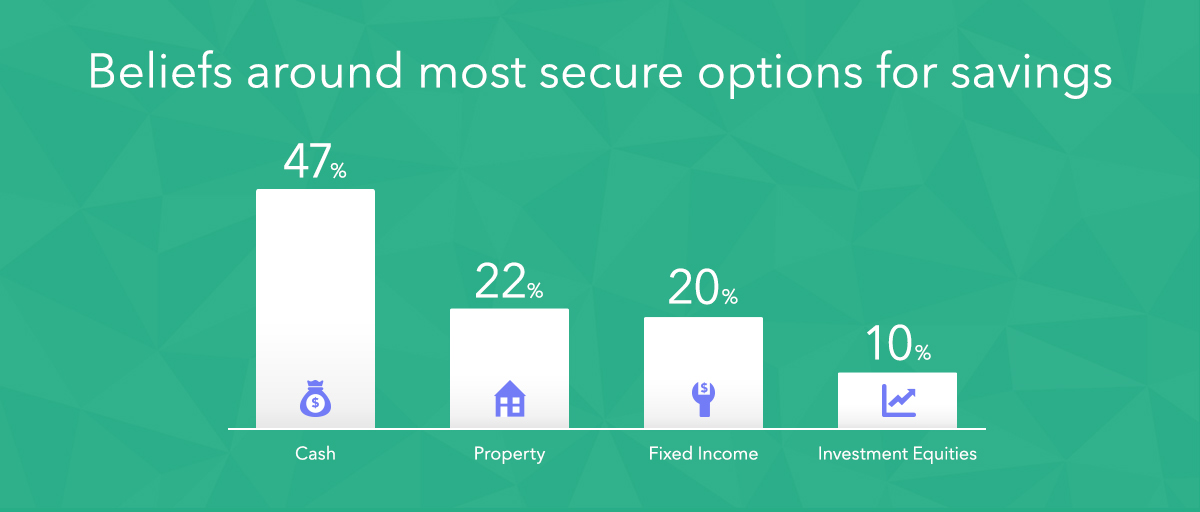

Even though your finances might be the last thing on your mind in your 20s, having a few financial goals will help lay the foundation for financial security in your 30s.

Of course, your goals will be different depending on your situation, however, these five can act as a place to start.

1. Know where your money is going

You’ve undoubtedly heard people harping on about making a budget. However, sticking to a budget doesn’t work for everyone. Even so, knowing where your money is going is incredibly important. This will help you understand where you could be spending less money and even where you could be making more money.

This could mean tracking your income and expenses in a spreadsheet or with an app, like Raiz. If you typically use a card to pay for things, these apps can sort your income and expenses into categories automatically. Ignoring your finances can land you in hot water, especially if you start accumulating credit card debt or “buy now pay later” debt such as with Afterpay.

2. Pay off high-interest debt

Many people have already dipped into high-interest debt, such as having a credit card or personal loan. However, these loans don’t have to be the end of the world. Paying off your debt goes hand in hand with knowing where your money is going. It’s important that you can meet minimum repayments every month, ideally going beyond this amount. Of course, you’ll also want to avoid getting into more debt.

3. Start investing your money

The thought of investing can be quite daunting, especially when you don’t know where to start. However, using a micro-investing platform such as Raiz makes it easy to invest in a diversified portfolio starting with $5. With Raiz, you don’t have to handpick stocks on your own. Plus, you can decide what level of risk you’re comfortable with. Over many years, you’ll see your money multiply with the power of compound interest and reinvested dividends. For more information on Raiz fees, click here.

If home ownership or property investment is a priority for you, now may be the time to buy, especially with the Australian market cooling. To comfortably afford repayments on a house in Australia, you’ll need to be making a significant amount. For example, in NSW, your household income would need to be $124,000 a year in order to avoid mortgage stress. You might consider setting an income goal or aim to save for a deposit in your 20s.

4. Have an emergency fund

Even if you’re not financially independent as of yet, having an emergency fund is always an important safety net to have. Usually, a 3-month emergency fund is enough in the case that you lose your job or decide you need time off work. Once you know what your monthly expenses are, multiply that number by three and aim to have this amount saved.

5. Take control of your retirement fund

Retirement should be many decades away. However, where your superannuation ends up is important now. Different super funds come with different fees and different historical returns. With compound interest, even a small difference can make you thousands more in the long-term.

After you choose a super fund that’s suitable for you, it’s important to make sure your superannuation is consolidated. Most people will have multiple jobs over their working life and sometimes this leads to having multiple super fund accounts that you’re paying fees for. Having all your money in one place will mean you’ll be making more with compound interest and only be paying one lot of fees.

Final words

For many people in their 20s, this is where you’ll enter your journey into financial independence. This means you’ll be developing habits that you’ll likely take into the rest of your life. Therefore, it’s more important than ever to make sure you’re building strong habits and goals so that you don’t end up having to reverse bad money decisions in your 30s.

Guest author: James Pointon is a Commercial Manager at OpenAgent.com.au, an online agent comparison website helping Australians to sell, buy and own property.

Don’t have the Raiz App?

Download it for free in the App store or the Webapp below:

Important Information

The information on this website is general advice only. This means it does not take into account any person’s particular investment objectives, financial situation or investment needs. If you are an investor, you should consult your licensed adviser before acting on any information contained in this article to fully understand the benefits and risk associated with the product.

A Product Disclosure Statement for Raiz Invest and/or Raiz Invest Super are available on the Raiz Invest website and App. A person must read and consider the Product Disclosure Statement in deciding whether, or not, to acquire and continue to hold interests in the product. The risks of investing in this product are fully set out in the Product Disclosure Statement and include the risks that would ordinarily apply to investing.

The information may be based on assumptions or market conditions which change without notice. This could impact the accuracy of the information.

Under no circumstances is the information to be used by, or presented to, a person for the purposes of deciding about investing in Raiz Invest or Raiz Invest Super.

Past return performance of the Raiz products should not be relied on for making a decision to invest in a Raiz product and is not a good predictor of future performance.

By Alison Banney from Finder.com.au

By Alison Banney from Finder.com.au