20 February, 2019

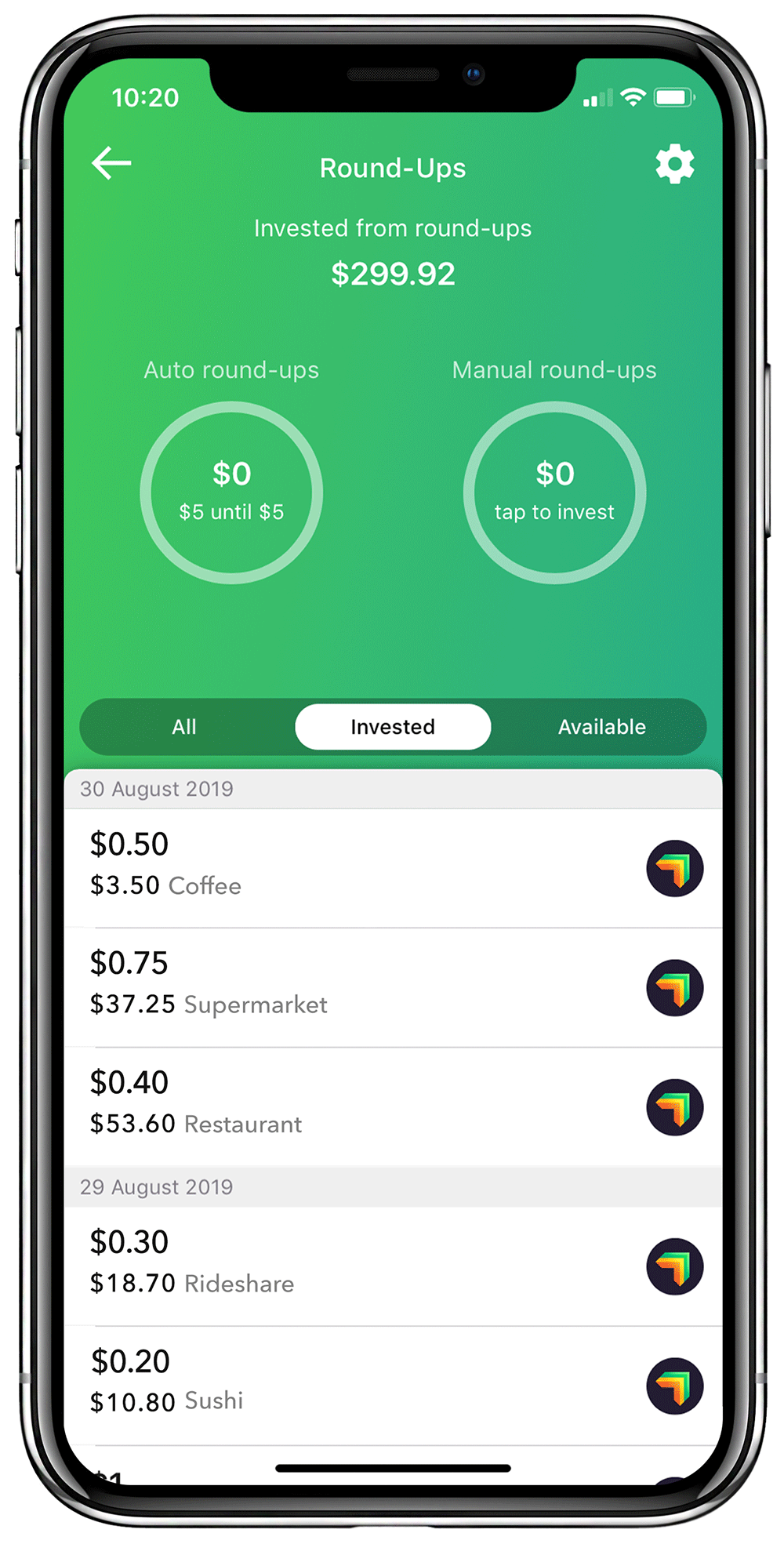

- An active Raiz Invest Account must be held (account balance greater than $5). Raiz account holders hold valid accounts as set out in the product disclosure statements found on the website: raizinvest.com.au.

- Entries open Thursday 21st February 2019 at 4PM and entries close Friday 1st March 2019 at 5PM. To enter, one must comment on the Facebook post within the time frame stated above.

- Raiz Invest will select five winners with a $100.00 credit investment in to their active Raiz Investment Account. These five investments will be selected at Raiz’s discretion. We note that no individual prize exceeds $250 and total value of prizes do not exceed $50,000.

- These five Raiz Account holders will be requested to message us their email and will be notified by email when the credit investment is deposited into their Raiz Investment account by Friday 15th March 2019.

- The permit number in the format NSW Permit No. LTPM/18/03853.

- This promotion is in no way sponsored, endorsed or administered by, or associated with any other third party.

- By entering this promotion, you agree that we may contact entrants or use entries for future marketing purposes in any media or branding.

- The competition is promoted by Raiz Invest Australia Limited, Level 11/2 Bulletin Place Sydney 2000 NSW, 1300 754 748. ABN 26 604 402 815, who is the Authorised Representative of AFSL 434776. The Raiz product is issued in Australia by Instreet Investment Limited (ACN 128 813 016 AFSL 434776) and promoted by Raiz Invest Australia Limited (ACN 604 402 815). A Product Disclosure Statement dated 10th April 2018 for this product is available on the Raiz website and App. A person should read and consider the Product Disclosure Statement in deciding whether or not to acquire and continue to hold interests in the product. The risks of investing in this product are fully set out in the Product Disclosure Statement and include the risks that would ordinarily apply to investing.

NSW Permit No. LTPM/18/03853